Market Snapshot

| Indices | Week | YTD |

|---|

On May 8th, leaders from across the global innovation economy will gather in Salt Lake City for the eighth annual ASU GSV SUMMIT, with the mission of accelerating exponential ideas in education and talent. We will welcome over 3,500 entrepreneurs, educators, business leaders, policymakers, and investors, as well as 350 game-changing presenting companies.

What makes the Summit so impactful is the unusual “cocktail” of participants we convene, with the common ingredient being a commitment to giving everybody an equal opportunity to participate in the future. Increasingly, as exponential ideas that are transforming other industries are applied to education — think Tesla’s impact on the automobile industry or Airbnb upending travel and hospitality — this goal is more reachable than ever.

We all go to conferences where there are some good speakers and intellectually stimulating conversation. But when you leave, it’s over. This is why the ASU GSV Summit has so much momentum. People come here because things happen here. Connections are made. Capital is raised. Ideas are brought to life. People come here to make things happen.

This year’s cocktail of keynote speakers includes LinkedIn CEO Jeff Weiner, acclaimed author Michael Lewis (Moneyball – 2003, The Blind Side – 2006, The Big Short – 2010, The Undoing Project – 2016), tennis great and education philanthropist Andre Agassi, transformational advocate Marian Wright Edelman, machine learning expert Andrew Ng (former Chief Scientist, Baidu + Chairman, Coursera), leading venture capitalists Joe Lonsdale (Founding Partner, 8VC + co-founder, Palantir), Tim Draper (Founder, Draper Associates + Draper University), Mike Maples (Founding Partner, Floodgate), and many others. (Disclosure: GSV owns shares in Coursera and Palantir).

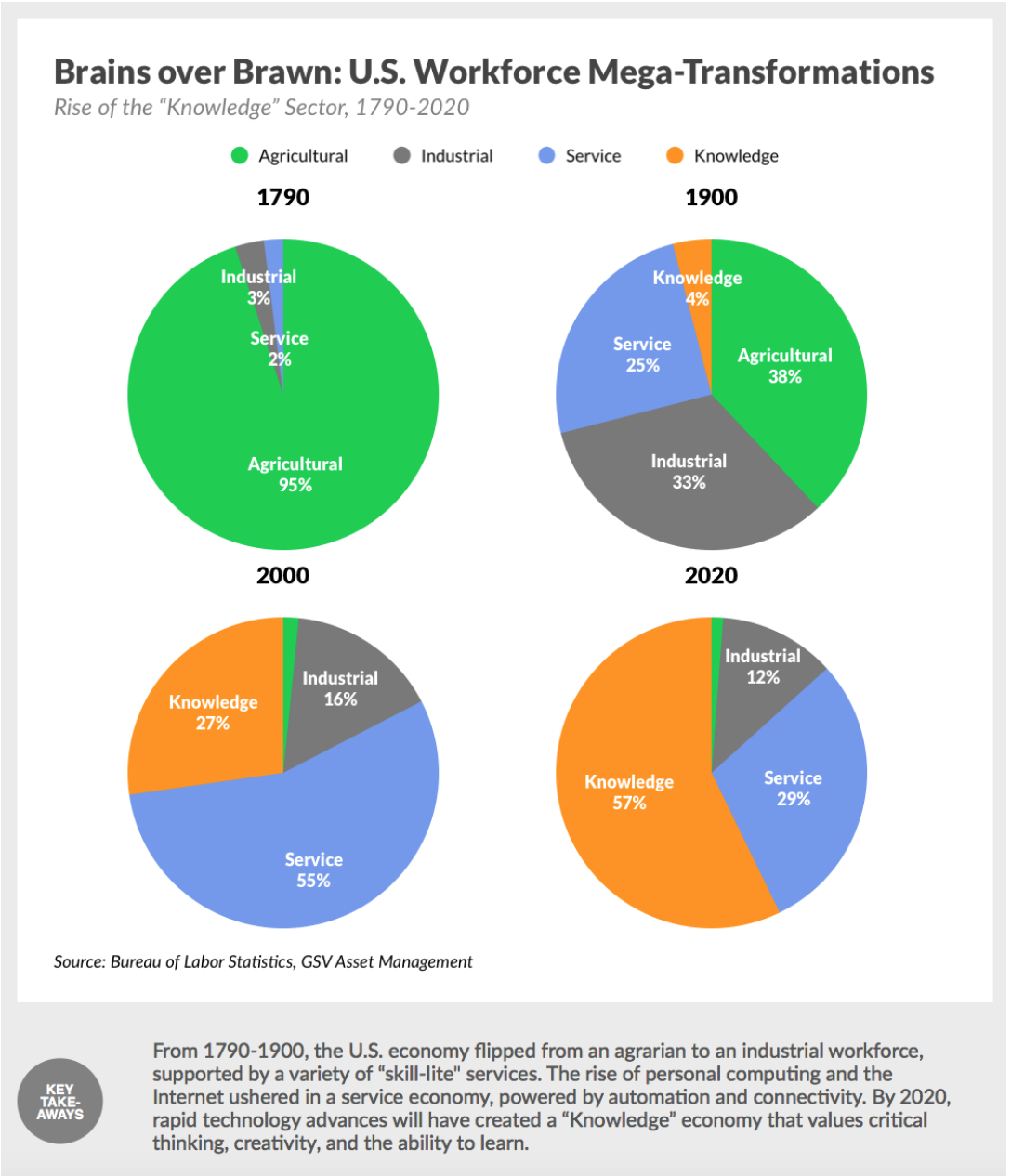

THE END OF HISTORY VS. THE FUTURE OF WORK

Throughout history, whether in pre-industrial or industrial times, great nations developed based on their access to physical resources or their ability to surmount physical barriers. England and Spain crossed oceans, Germany turned coal and iron into steel, and the United States exploited a wealth of agricultural and industrial resources to become the World’s breadbasket and industrial superpower.

But the advent of the personal computer, the Internet, and the digital delivery of information shifted the World’s focus from physical capital to human capital. The most valuable resources in a physical economy are commodities like coal, iron, and oil. Their value is judged by metrics like purity and volume. In a knowledge economy, the most valuable resource is talent. Talent is valued based on brainpower, and the ability to acquire, deliver, and process information effectively.

The Service Economy that developed after World War II started to shift education requirements. If you wanted to participate in the service industry — in jobs ranging from accounting to retail sales to entertainment — some formal education was required. Brains started to win out over brawn.

Gaining knowledge was worthwhile; these jobs were safer, less strenuous, and often better paid. Nevertheless, the education demands were still fairly low: in 1950, roughly 20% of the rising U.S. workforce had some college education by age 30, and only 20% of jobs required a postsecondary credential.

The Personal Computer revolution that began in the mid-1970s displaced a wide range of manual labor, administrative, and clerical jobs — many that were lucrative and desirable. The World changed again when Netscape debuted on Wall Street in 1995. Broadband Internet connectivity transformed communication, making an individual’s actual workplace less relevant.

Now, U.S. workers faced competition not only from computers, but also from low-cost talent pools thousands of miles away. One click and you were connected to your service representative in Mumbai. In developed countries, knowledge work became the new area of opportunity.

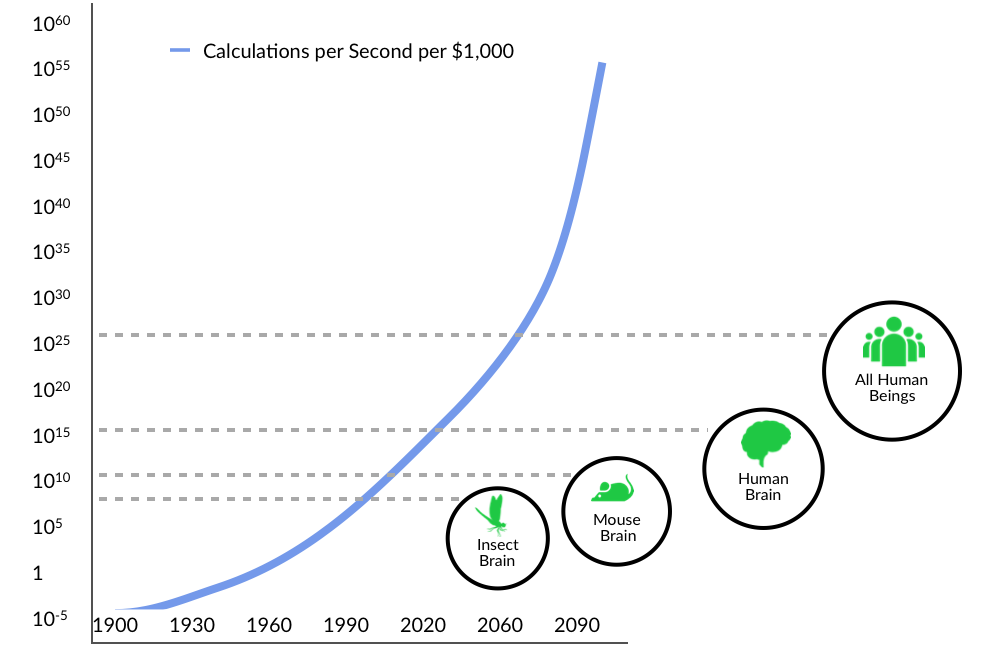

Today there is a prevailing sense that rapidly accelerating digitization and automation is triggering an economic shift unlike any we have seen before. As MIT scholars Erik Brynjolfsson and Andrew McAfee observe in The Second Machine Age, an unsettling future is taking shape characterized by massive unemployment and economic disruption stemming from the fact that as computers get more powerful, companies will have less need for workers of any kind.

Oxford researchers have projected that 47% of American jobs are at “high risk” of being automated in the next 20 years. McKinsey estimates that 12 million U.S. “middle skill” jobs will be eliminated by 2025. Globally, there are over 350 million manufacturing and warehouse workers — roles that are rapidly being replaced as companies like Amazon, which already “employs” 30,000 warehouse robots, seek low-cost, high-efficiency alternatives to human labor. A White House economic report predicted that 83% of jobs that pay less than $20 an hour will be eliminated by automation.

Through the automation eliminating traditional jobs, Bank of America Merrill Lynch predicts that there will be a $9 trillion reduction in employment costs. Additionally, AI technologies could reduce $8 trillion of costs in the manufacturing and healthcare industry and creating $2 trillion of efficiency gains through autonomous vehicles and drones. All in all, the annual disruptive impact of AI technologies could amount to up to $33 trillion.

What does that all amount to? According to the McKinsey Global Institute, The AI revolution is transforming society 10x faster, at 300x the scale, and approximately 3000x the impact of the Industrial Revolution.

White collar jobs of all types are are up against major challenges. By 2025 it’s estimated that $7 trillion will be managed by robo-financial advisors. The Associated Press is already using Artificial Intelligence to produce over 3,000 financial reports per quarter. Effectively, robots are managing money and reporting financial results.

For many, it feels like technology jobs are an Alamo.

It’s why Mark Zuckerberg said. “Our policy is to hire as many talented computer engineers as we can find. There aren’t enough people who have these skills today.” It’s why the U.S. Department of Labor projects there will be 1.2 Million computer science related job openings by 2020. No less an authority than the Harvard Business Review recently called Data Science, “The sexiest job of the 21st century.”

The problem is that we are living in exponential times. The computer capability curve is getting steeper. Technology replaces the technologist. Automation is going from Blue Collar, to White Collar, to “No Collar”.

It’s why you’re hearing a chorus of people claim the end of times is here. Nobel laureate Paul Krugman has speculated that, “We could be looking at a society in which all the gains in wealth accrue to whoever owns the robots.” Y-Combinator’s Sam Altman has suggested that, “The obvious conclusion is that the government will just have to give [unemployed] people money.”

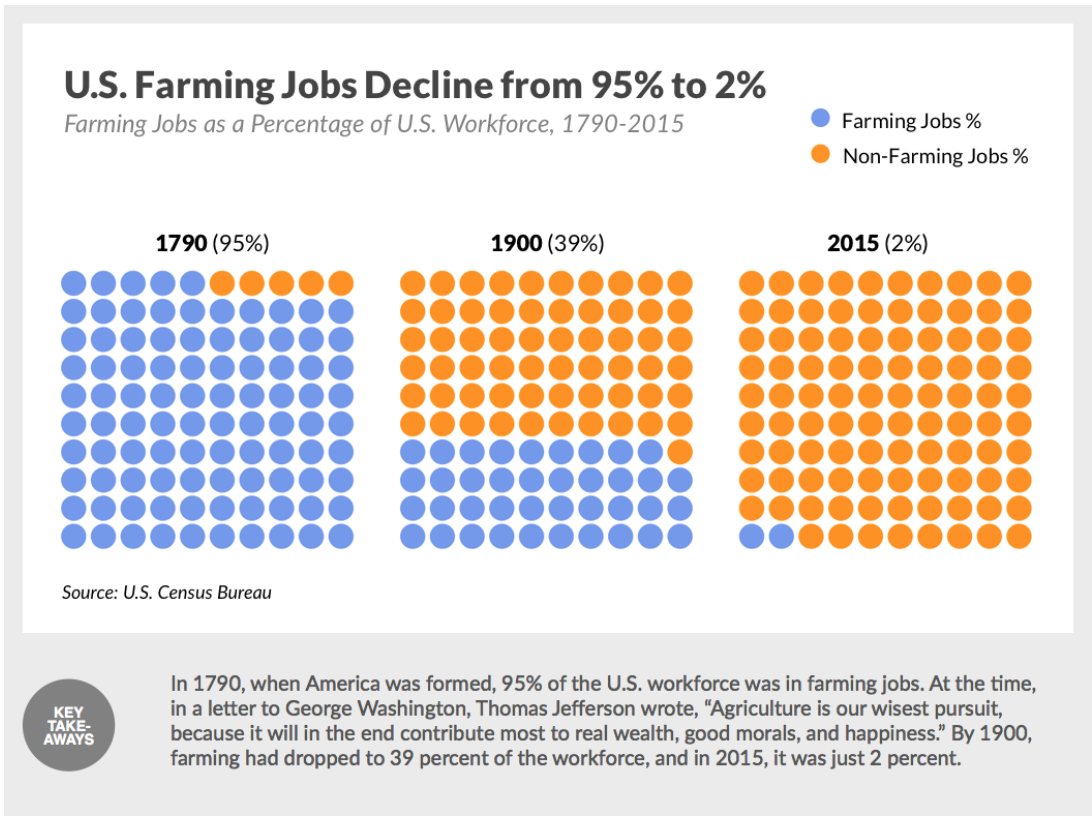

Aside from the minor issue that the government doesn’t make money — it takes money — one thing we know as sure as the Sun coming up in the East is that automation eats jobs. But it doesn’t eat work. In 1787, Thomas Jefferson observed that, “Agriculture is our wisest pursuit, because it will in the end contribute most to real wealth, good morals, and happiness.” We know how that played out.

We don’t think that we’ve reached the end of history. We just need to think differently.

Imagine how farmers would have responded if you told them in 1790 that essentially all of the agricultural jobs were going to vanish in less than two hundred years — or, in other words, that the entire agrarian economic ecosystem was going up in smoke. Many would have lobbied the government to protect their livelihood. Others might have shrugged off the news, betting that it wouldn’t happen on their watch. But indignant, indifferent, or ignorant, change happens.

ATMs were introduced to banks in the 1970s and their numbers in the U.S. quadrupled from roughly 100,000 to 400,000 between 1995 and 2010. You might assume that these machines spelled the end of bank work.

But U.S. bank teller work actually rose modestly in this period from 500,000 to approximately 550,000 over the 30-year period from 1980 to 2010. As David Author notes in his piece “Why Are There Still So Many Jobs?” (Journal of Economic Perspectives, 2015) ATMs reduced the cost of operating a bank branch. Tellers per bank fell, but the number of branches surged by 30%. At the same time, branch bankers shifted their focus from routine cash handling to human interactions, forging lifelong, multi-product relationships with customers.

2017 ASU + GSV SUMMIT: THE FUTURE OF EDUCATION & TALENT IS NOW

Kaizen is a Japanese business term meaning “continuous improvement.” An education corollary is GSV’s concept of “KaizenEDU,” which means “continuous learning.” In a world with smart machines, you can no longer fill up your “knowledge tank” until age 25 and cruise through life. Effective workers must refill their knowledge tanks continuously.

At this year’s ASU GSV Summit, we’re going to hear from innovators of all stripes — from entrepreneurs, to policymakers, business leaders, educators and investors — who are “thinking differently” to make KaizenEDU a reality.

That means applying transformational technologies to learning, including Big Data and Artificial Intelligence. It’s scaled platforms that are reaching millions of people with engaging and effective education opportunities — what we call “Weapons of Mass Instruction.” It’s new models that help people get the skills they need without dropping out of life and taking on massive debt.

Below is a full agenda for the Summit, which you can also access HERE. We hope to see you there!

52716.png)

Additional Programming on Monday, May 8th

- The Future of Work is Now! (view HERE)

- Leading Educator Program (view HERE)

- Pre-K to 12 Program (view HERE)

- Post-Secondary Program (view HERE)

- Global Program (view HERE)

- Venture + Growth Company Presentations (view HERE)

76067.png)

Additional Programming on Tuesday, May 9th

- The Future of Work is Now! (view HERE)

- Leading Educator Program (view HERE)

- PreK to 12 Educator Program (view HERE)

- Post-Secondary Program (view HERE)

- Global Program (view HERE)

- Venture + Growth Company Presentations (view HERE)

96179.png)

Additional Programming on Wednesday, May 10th

- The Future of Work is Now! (view HERE)

- Leading Educator Program (view HERE)

- PreK to 12 Program (view HERE)

- Post-Secondary Program (view HERE)

- Venture + Growth Company Presentations (view HERE)

(Disclosure: GSV owns shares in Chegg, Knewton, General Assembly, Clever)