Market Snapshot

| Indices | Week | YTD |

|---|

These things will not bite you, they want to have fun. Then, out of the box came thing two and thing one!

— Dr. Seuss, The Cat in the Hat

My good friend Bill Campbell used to say, “You’re as dumb as a post” to our football team. Soon, posts won’t have to be dumb.

To anybody under the age of 30, it’s not a “smartphone”… it’s a phone. You expect to have a computer in your pocket. Never mind that it’s more powerful than the computers NASA used to land the first astronauts on the moon.

In his 1995 book Being Digital, Nicholas Negroponte argued that technology would transform our world — down to the everyday objects that surround us. He foresaw a future where atoms are relentlessly transformed into bits. It’s remarkable how prophetic he was.

Atoms make up physical, tangible objects such as CDs, books, and newspapers. Bits are the smallest unit of information on a computer. They have no color, weight, or size, and can travel at the speed of light.

Being Digital argues that everything physical will ultimately become digital… that atoms get replaced by bits.

This prophesy has played out in phases. Its evolution can be traced through the rise of Amazon, which began by distributing physical items digitally (e.g. Books), and now distributes digital items digitally (e.g. eBooks).

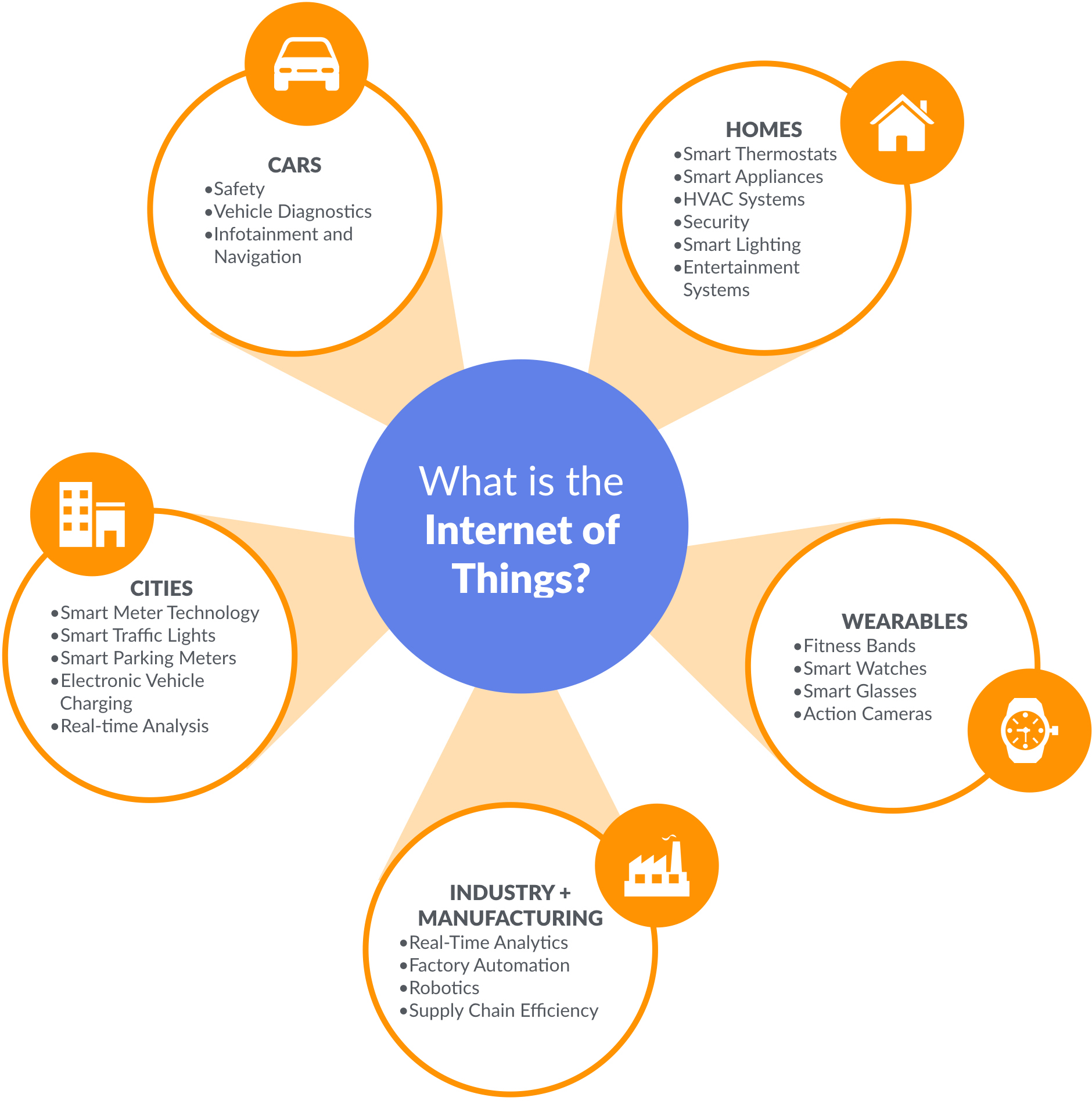

But an interesting twist to Negroponte’s paradigm is emerging. As we embed chips in physical devices to make them “smart,” bits and atoms are co-mingling in compelling ways. Collectively called the Internet of Things (IoT), connected devices are appearing in our homes, on the highway, in manufacturing plants, and on our wrists. Estimates vary widely but IDC has predicted that the IoT market will surpass $1.7 trillion by 2020.

Here again, Amazon’s arc is instructive. Its “Echo” smart speaker, powered by a digital assistant, “Alexa”, has sold over three million units in a little over a year. Echo enables users to play music with voice commands, as well as manage other integrated home systems, including lights, fans, door locks, and thermostats.

Source: The Verge

The “Internet of Things” is effectively a catch-all for connecting devices — from consumer objects to industrial equipment — onto a network. This enables information gathering and remote device management via software to increase efficiency. It also enables the creation of new services, to achieve, health, safety, business, or environmental benefits.

STATE OF PLAY

The Internet of Things entered the public consciousness in recent years with the rise of wearable devices focused on health and wellness, led by Fitbit. Today, the company counts more than 20 million users and Forbes projects that over 400 million wearable devices will be sold per year in 2020, worth $34+ billion.

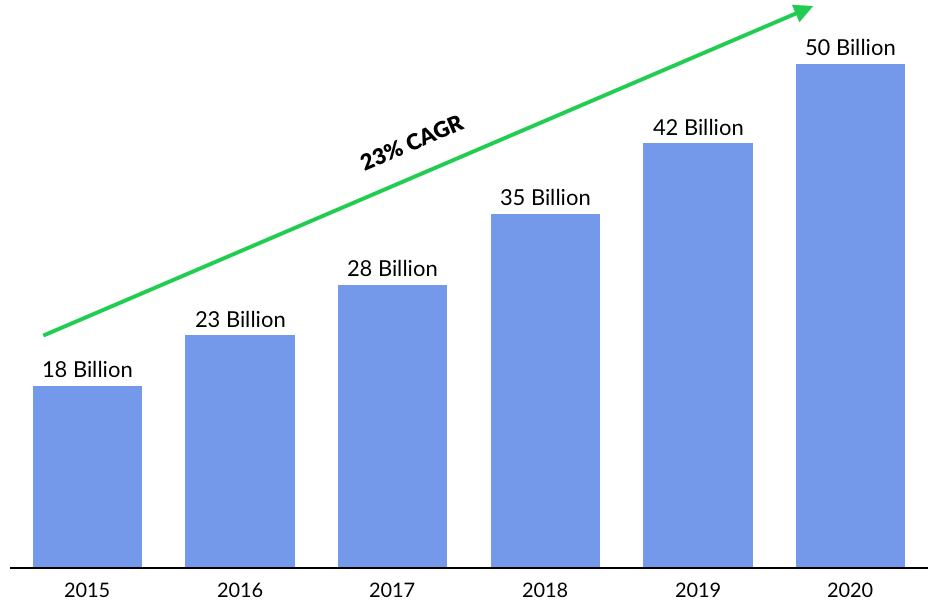

But increasingly, anything than can be connected will be connected. Accordingly, we’re poised to see a rapid proliferation of IoT devices. Today, Cisco estimates that there are 18 billion such devices, growing to 50 billion by 2020.

As a result, chipmakers are making massive bets on IoT to meet surging demand for connected devices.

In June, Samsung announced a $1.2 billion U.S. initiative to broaden its IoT capabilities — from chips to a range of connected products — over the next four years. A month later, SoftBank broke the bank with a $32 billion acquisition of ARM Holdings, which licenses chips used in smartphones, as well as an increasing number of Internet-connected domestic appliances. Earlier, in February, Cisco completed a $1.4 billion acquisition of Jasper Technologies, a software developer that allows businesses to manage everything from beer kegs to vending machines, cars, and security systems.

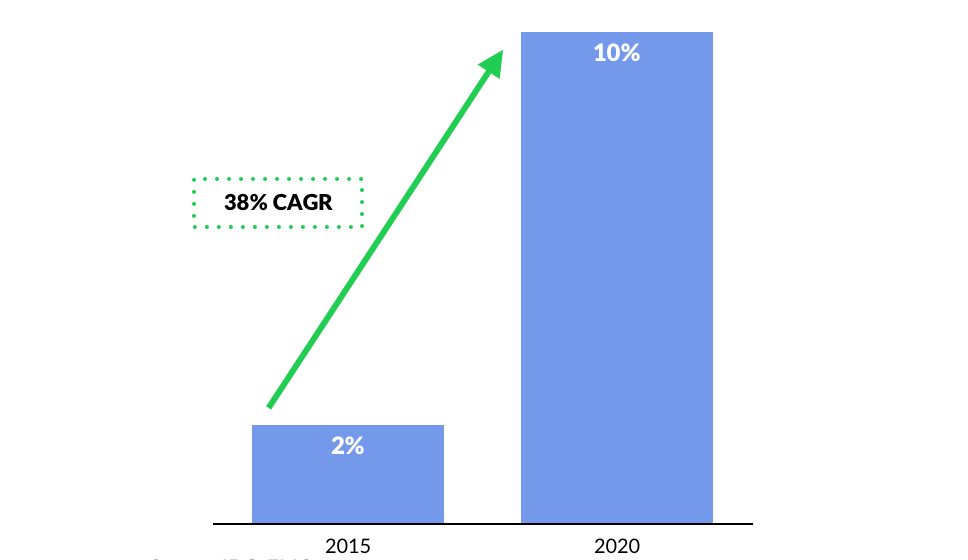

The surge in devices is driving a massive output of information, an impact that is already visible in the digital universe. Data from embedded systems — the sensors and systems that monitor physical objects — already accounts for 2% of global data usage. By 2020 it is projected to increase 5x.

Financing Activity

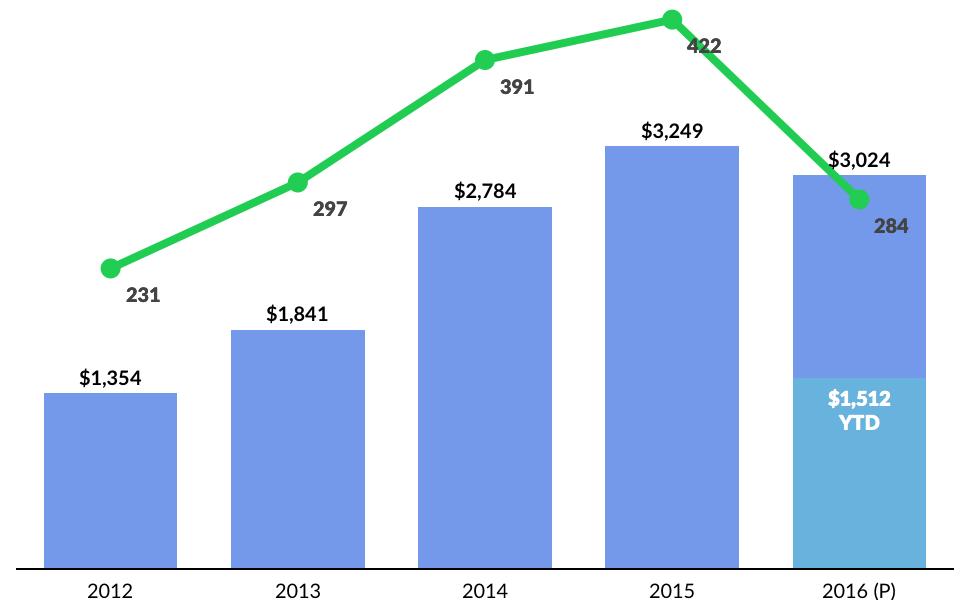

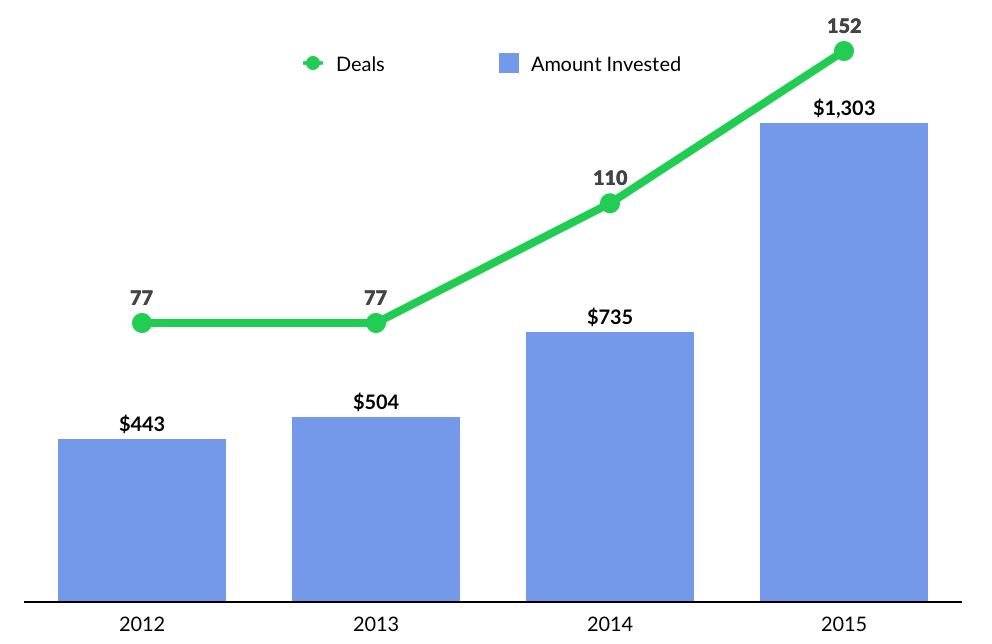

Between 2012 and 2015, VCs invested over $9 billion in IoT businesses across 1,300+ deals. During this period, annual funding grew from $1.4 billion to $3.2 billion, representing a 34% compound annual growth rate (CAGR). But the pace of dealmaking has cooled off in recent months. Funding sank from $837 million in Q1 2016 to $656 million in Q2, and activity fell from 75 deals to 62.

Notable 2016 financings include gaming hardware maker Razer ($75 million Series C), smart doorbell Ring ($61 million Series C), IoT platform Ayla Networks ($39 million Series C), smart thermostat Tado ($23 million Series C).

In March, GSVlabs hosted an IoT innovation showcase, with a group of 25 emerging IoT and connected home startups, including Automatic Labs, Center Electric, and SIGFOX. We expect this ecosystem to expand as disruptive businesses continue to proliferate and investors seek them out. (Disclosure: GSV owns shares in GSVlabs)

OBJECTS VS. SERVICES: THE LESSON FROM CARS

The automobile industry offers two key lessons for the future of IoT.

First, services are more important than objects. Uber and Lyft effectively make any car “smart” because anyone with an iPhone can plug their vehicle into a network that connects passengers with drivers. At some point, the current fleet of cars will be replaced with even “smarter” autonomous vehicles. But what consumers care about is that they can access affordable, efficient rides. Connected objects are less important than the compelling service they provide or enable.

The second lesson is that increasingly, it will be table stakes for objects to be “smart.” It’s a redundancy. Anything with a chip can be “connected.” Insanely good products, as always, will make the difference.

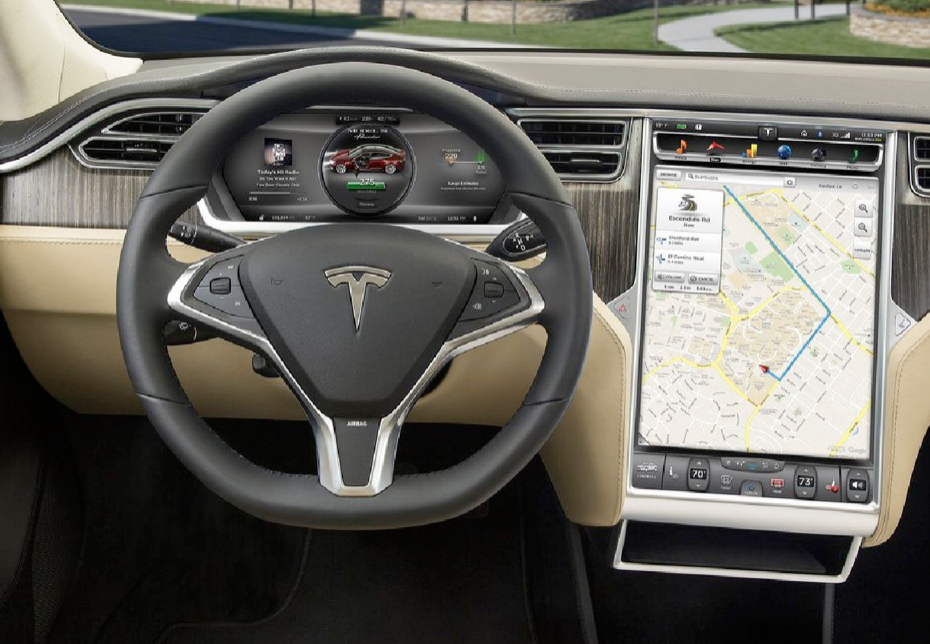

This week, Tesla announced improvements to its 0-60 acceleration and battery life that underscore how much the company’s vehicles break with precedent. Teslas are not cars with chips. They are computers on wheels.

For example, Teslas uses Big Data analytics to anticipate problems and improve performance. The Model S runs constant calculations to estimate how much charge is available on a driver’s battery. Battery range factors in a variety of data collected in real-time, including route terrain, outside windspeed, and driver usage patterns. The car continuously monitors its distance from the nearest supercharger, and notifies drivers before they go out of range.

Meanwhile, improvements to speed, battery function, and handling, can be downloaded as Tesla releases software updates. Going from a Tesla to a regular car is like switching back to a flip phone.

EMERGING OPPORTUNITIES

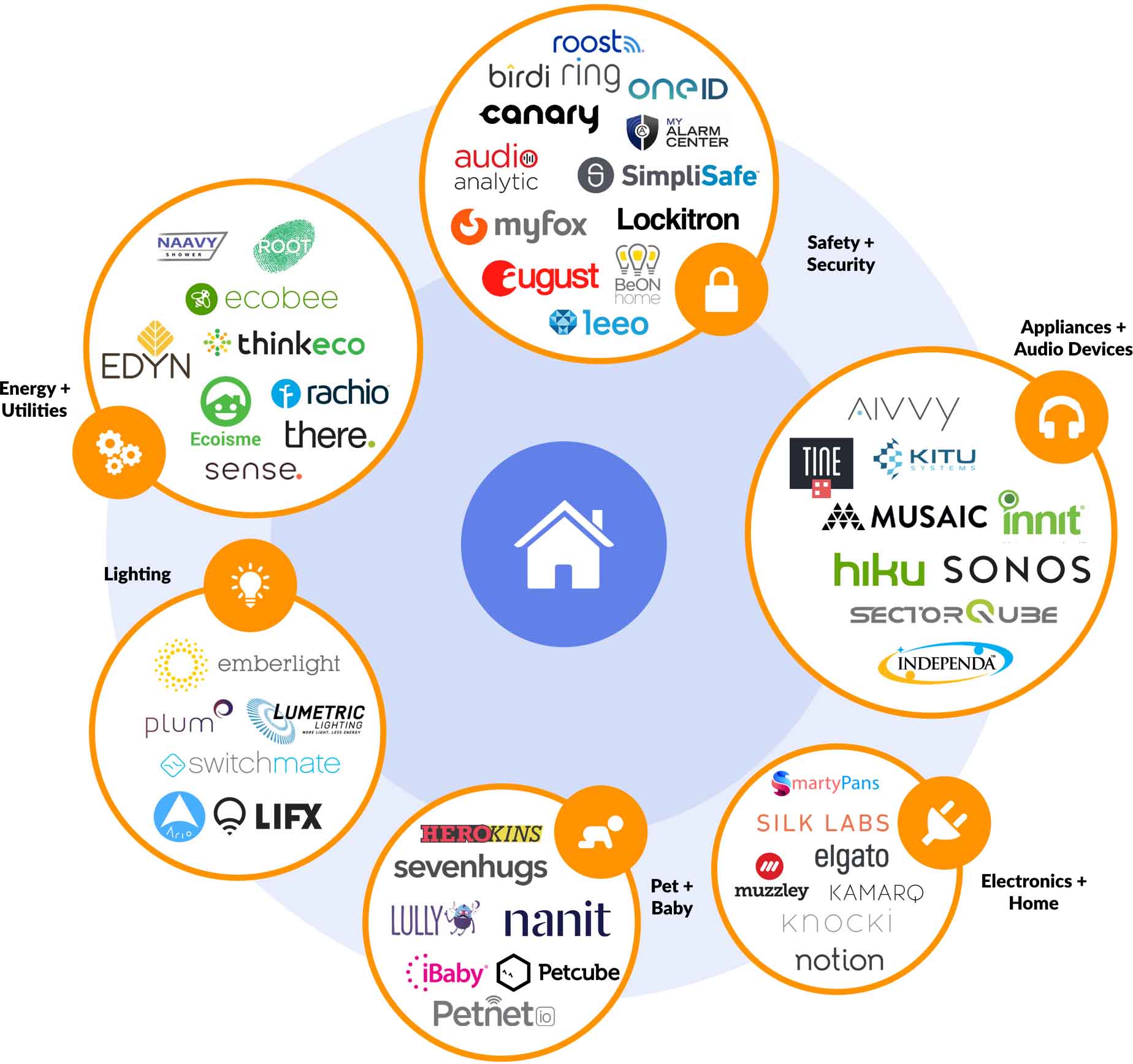

Smart Home

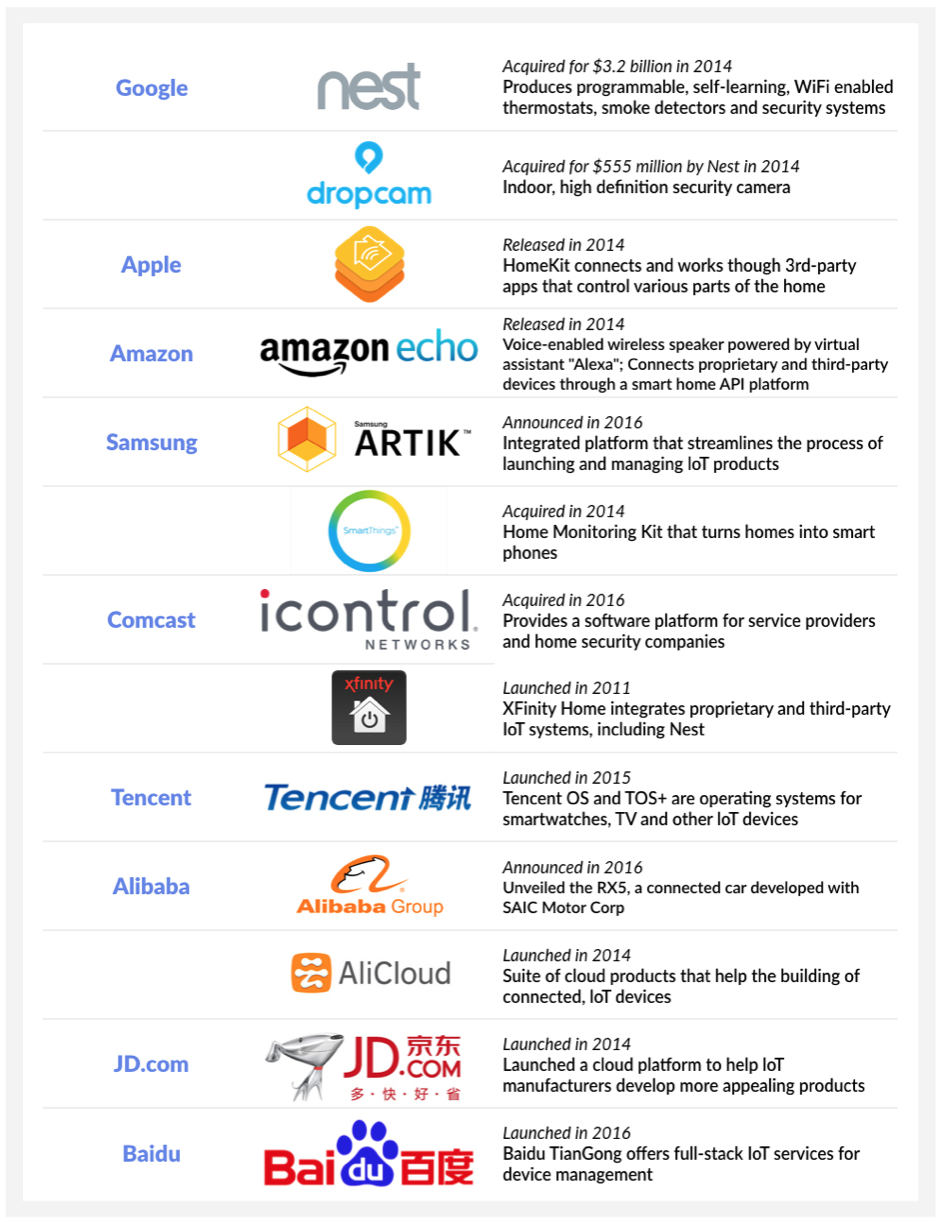

Google’s (Alphabet) $3.2 billion acquisition of Nest, the smart thermostat maker, in 2014 signaled the beginning of a land grab for the connected home. Later that year, it bought Dropcam, a home security camera maker, for $550 million.

As the Economist has reported, Nest has undoubtably been a disappointment to date for Google. It sold just 1.3 million units in 2015, and only 2.5 million in total over the past few years. Nest founder Tony Fadell stepped down in June amid reports that he had a much broader and aggressive vision for the product than Google was willing to pursue.

Nest’s problems are symptomatic of IoT for the home more broadly. According to Forrester, only 6% of American households have a “smart” home device, including internet-connected appliances, home-monitoring systems, speakers or lighting.

But as isolated offerings evolve into integrated, compelling services, the opportunity is open-ended. Major technology companies have taken notice, rolling out a variety of offerings to network key aspects of your home.

Though still off the peak seen in 2014 when Google acquired Dropcam and Nest, funding to smart home startups has accelerated in 2016. According to CB Insights, in 2015, VCs invested $404 million in smart home startups across 81 deals. This year will likely close with over $800 million invested across roughly the same deal count.

Industrial IoT

While the consumer adoption of fitness bands and connected household appliances might generate more media buzz, the potential for adoption by businesses may be much greater. Research from the McKinsey Global Institute suggests that the operational efficiencies IoT affords will create economic value measured in the trillions across industries. Think factory automation, real-time production analytics, and supply chain efficiencies.

Investment activity is following the opportunity. Notable 2016 financings include IoT platforms Greenwave Systems ($45 million Series C) and Ayla Networks ($39 million Series C), commercial 3D printing company Desktop Metal ($34 million Series C), commercial drone developer Airware ($30 million Series C), IoT analytics company Maana ($26M Series B), and connected HVAC and lighting company Enlighted ($25 million Series D).

THE POWER OF THE PLATFORM

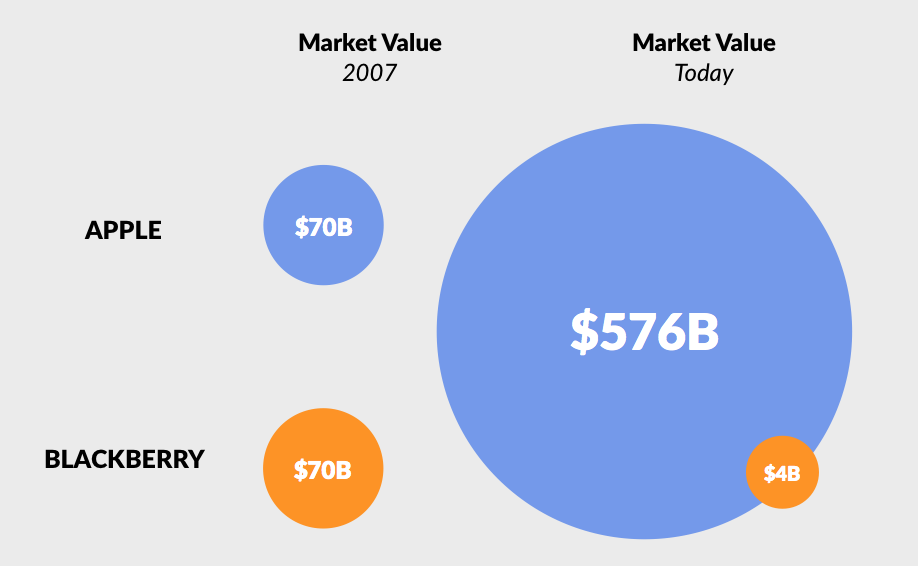

It wasn’t too long ago that BlackBerry was the coolest technology company in the World. In fact, people were so addicted to their BlackBerries that they were called “Crackberries.”

In 2007, BlackBerry and Apple were both roughly $70 billion market value businesses. Then Apple launched the iPhone. Today, Apple’s value has ballooned to over $576 billion, while BlackBerry has decreased more than 90 % to $4 billion.

What happened?

A major part of the story is that Steve Jobs and the Apple TEAM created an insanely great product. The iPhone is a beautiful device with the first viable multi-touch screen interface.

But the critical innovation was Apple’s unprecedented open mobile operating system, iOS, which enabled third-party developers to easily create apps for the device — effectively harnessing the wisdom of crowds to create a rich user experience. Apple created a platform.

Unlike BlackBerry, Apple had an army of outside developers who had already built consumer apps for its computers and iPods and were primed to do the same for the iPhone. By the time BlackBerry launched its first app platform in 2009 — a full two years later — iPhone customers had already downloaded one billion apps.

Recognizing that having a platform was the key to competing for the future of mobile — and by extension, gaining access to a broad consumer activity set — Google launched its Android operating system shortly after the release of the iPhone. Today, iOS and Android power the mobile World and there have been over 226 billion app downloads to date.

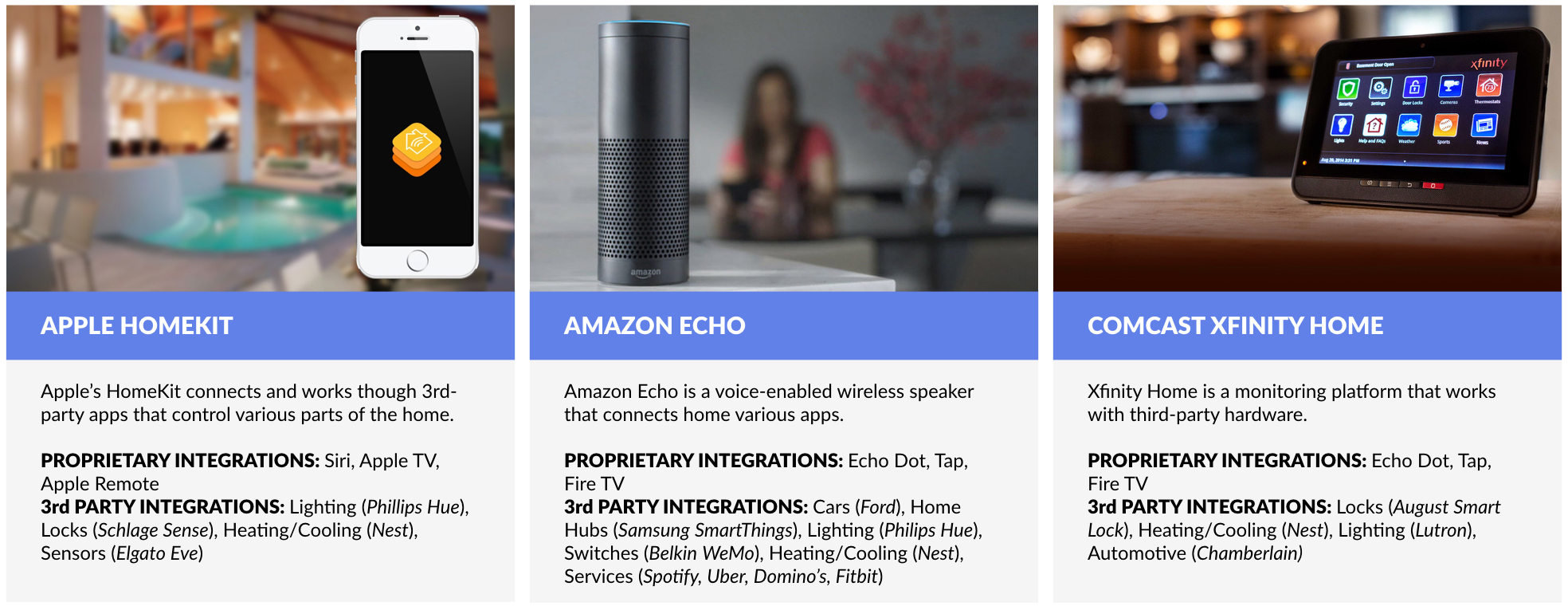

As with the smartphone, we’re seeing early signs of platform wars around IoT. Apple’s HomeKit, for example, aims to connect a range of proprietary and third-party smart home devices through an integrated control panel. Amazon recently released an open API framework to enable the integration and management of other devices through its voice-controlled Echo product.

WHAT’S NEXT

In July 2015, the world received a stark example of what hacking looks like in a World where digital and physical boundaries are blurred.

To illustrate the risks, a Wired reporter took the wheel of a Jeep Cherokee while hackers activated the windshield wipers, blasted the radio and air conditioning, and disengaged the car’s transmission while sitting in a basement ten miles away. Within days of the story breaking, Chrysler recalled 1.4 million vehicles that were susceptible to the same kind of attack through the company’s “Uconnect” dashboard computers.

Physical assets — from power plants to subway systems — have grown vulnerable to cyber attacks as key aspects of their operation have been digitized and networked.

While these high-profile attacks on large targets have rightfully caused alarm, a much larger threat is emerging by virtue of a rapidly proliferating ecosystem of Internet-connected devices — the Internet of Things (IoT) — that extends beyond computers, phones, and tablets into wearable devices, thermostats and washing machines.

Adding Internet connectivity to everything multiplies vulnerabilities. IoT devices effectively enable sophisticated attackers to move laterally across a network after they gain an entry point. In other words, hackers can infiltrate one device and start probing an entire system until they find a high-value database of personal information or a repository of sensitive business data.

At the core of this challenge is the fact that the proliferation of Internet-connected devices has been fueled by the availability of low-cost, mass-produced semi-conductors which can be embedded in anything. Chipmakers and device producers are both highly incentivized to keep costs down, which has resulted in underinvestment in security capabilities — from encryption to secure booting.

The widespread availability and proliferation of these devices means that once a device is compromised, it’s very difficult for a company to flip a switch and correct the problem.

Compounding the issue is that the surge in connected devices is being catalyzed by young companies that often lack the talent and resources to embed World-class security infrastructure in their products.

Gartner estimates that by 2017, more than half of all IoT products and services will be developed by companies less than three-years-old. And while some of these newcomers are likely to have formidable technical expertise, many will lack the ability to implement viable security mechanisms.

Industry groups like the International Standards Organization (ISO), the Thread Group, the Open Interconnect Consortium, the AllSeen Alliance, and the Industrial Internet Consortium have all turned their attention to dramatically improving security standards in connected devices.

These efforts will accelerate as consumers increasingly understand the yawning security gaps in the World of IoT.

—

Stocks had a lazy week, which was fitting for the final gasp of Summer. NASDAQ took its first nap in seven weeks and was off 0.4%. The S&P 500 fell 0.7% and the GSV 300 was down 0.1%. Oil prices dropped 3% last week, falling below $50, but new home sales shot up 12%.

Fed Chairman Yellen yodeled from the mountains of Jackson Hole that it looks like rates are heading upward. Her Vice Chairman, Stanley Fischer, put an exclamation point on her remarks and said we should expect a few rate hikes before the new year.

Walmart got back to its old ways, inflicting pain on competitors. Dollar Tree and Dollar General both fell over 10%, hurt by the boys from Bentonville. Best Buy roared back from the dead with surprisingly strong results and its shares soared 21% for the week.

Workday popped revenues 34%, and despite larger losses than Wall Street forecasted, its shares rose for the week. Tesla continued to show that it was effectively a computer on wheels, with upgrades providing quicker 0-60 acceleration and longer battery life.

We remain BULLISH on the outlook for premier growth companies, and accordingly, continue to be BULLISH on buying leaders such as Facebook, Google, Amazon, Tencent and Alibaba.