Market Snapshot

| Indices | Week | YTD |

|---|

This week leaders of the G-20 nations met in Hamburg, Germany, but if you read the headlines, you might have mistaken the summit for a primetime prizefight between President Trump and Vladimir Putin. The much-hyped meeting obscured an agenda focused on global economic growth.

When it comes to one key indicator of economic growth — stock market performance — Russia actually offers an useful lens to view the global state of play. Equities in Russia have tumbled in 2017 — the flagship RTSI index was down nearly 16% at the end of the second quarter — while stock markets in almost every other G-20 nation have risen, and in many cases surged.

As of June 30, the S&P 500 was up 8.2%, NASDAQ had risen 14.1%, and the Dow had gained 8.0%. China’s SSE Composite Index was up 2.9%, Hong Kong’s Heng Seng has jumped 17.1%, and India’s Sensex was up 16.1%. As what might be a preview to future opportunities, the GSV 300, which is made up of 300 of the fastest growing companies in the World was up a whopping 26.6% in the first half.

The most relevant index for Institutional Investors to date has been the S&P 500, which is a good proxy for broad Market dynamics. But with a 7% long term growth rate, it hardly reflects conditions or performance for fast growing companies.

The fact that the S&P 500 is solely a market cap weighted index is problematic in that a $100 Billion Market Cap Company has 100x the impact on the Index as a $1 Billion Market Cap Company… not realistic in that a portfolio manager who viewed two portfolio companies as being equally attractive would have 100x more of that company in their portfolio.

The most well-known index, the Dow Jones Industrial Average (DJIA), is created with an even more bizarre rationale in that it is weighted by share price. So in other words, if one stock was $30 per share and another was $300 per share, the $300 stock would have 10x the influence on the DJIA as the $30 stock.

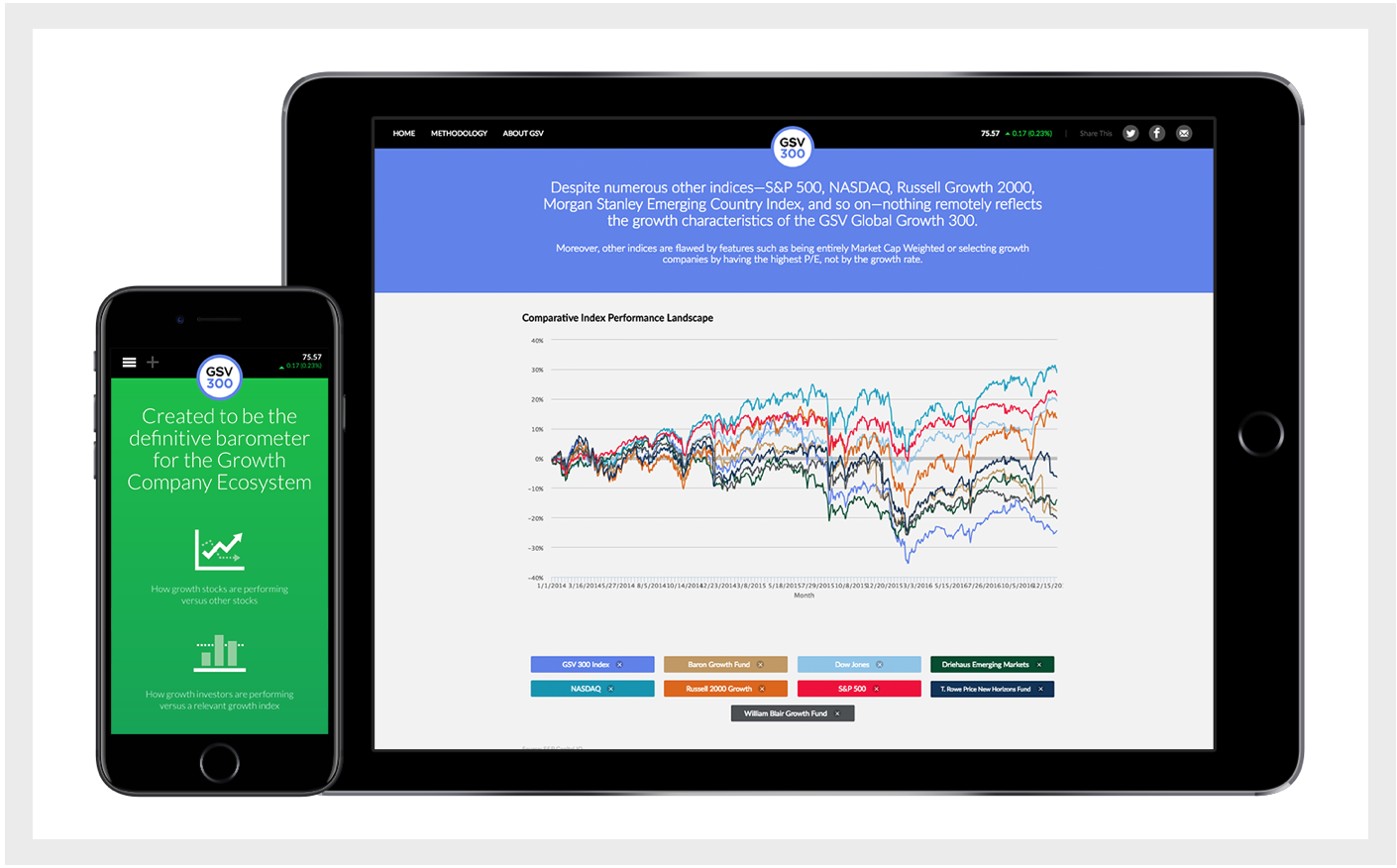

In 2015, GSV launched the GSV 300 Index, which we believe is the best representation of what is truly going on with growth companies, their valuations, and performance. It is an index of 300 of the World’s fastest growing companies, selected systematically based on key fundamentals, including revenue and earnings growth, geography, valuation metrics, and market capitalization.

The GSV 300, by contrast, is constructed using a systematic three-step process, which is summarized below: Screening, Ranking + Scoring, and Index Weightage. For a full description of the GSV 300 construction methodology, please click HERE.

The average market capitalization of GSV 300 constituent companies is $7.0 billion, with a median of $1.6 billion. The 10 largest companies account for 25% of the index. By comparison, the top five companies in the 2,500-company NASDAQ Composite — Apple, Microsoft, Amazon, Facebook, and Alphabet (Google) — account for over 30% of the index alone.

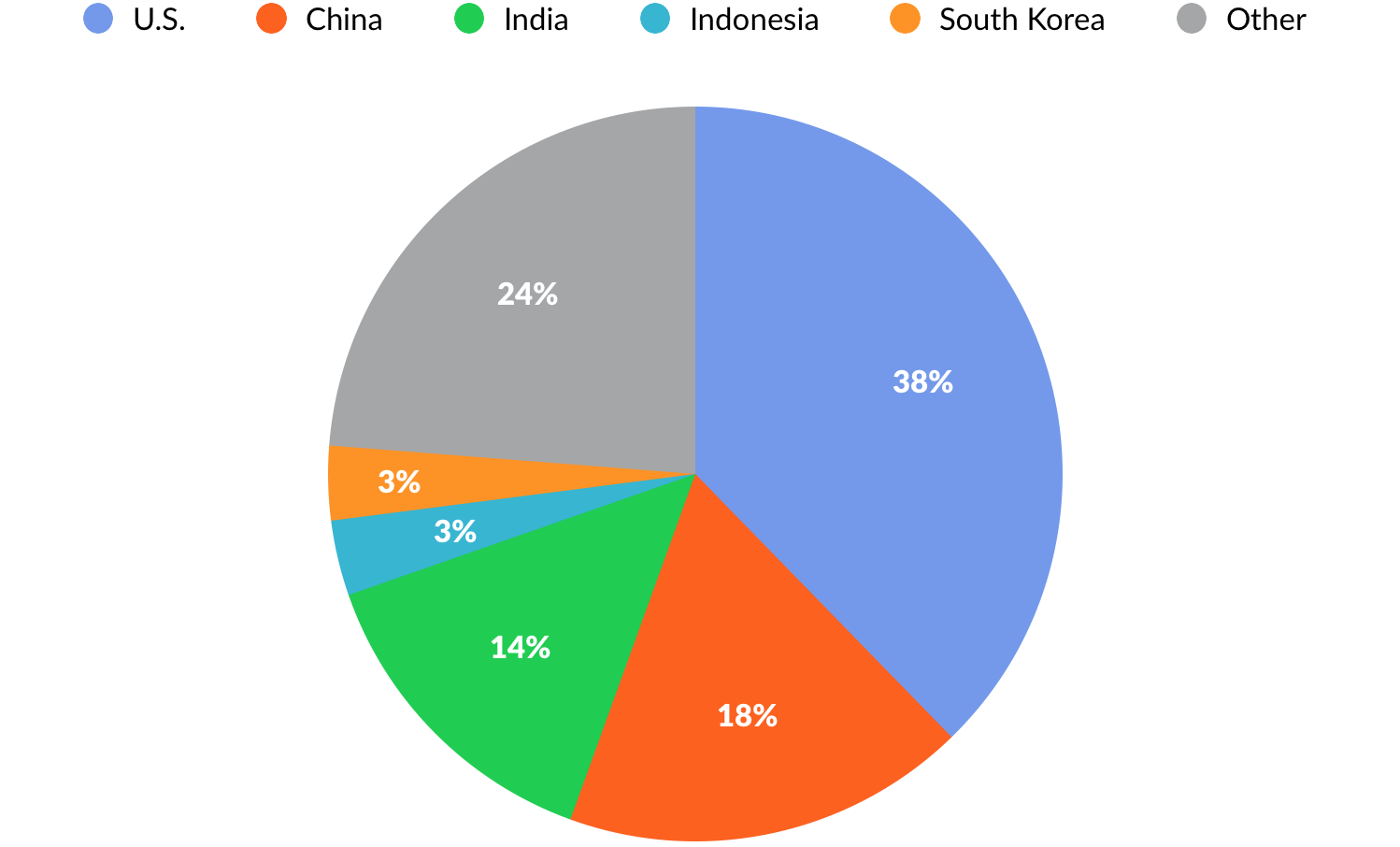

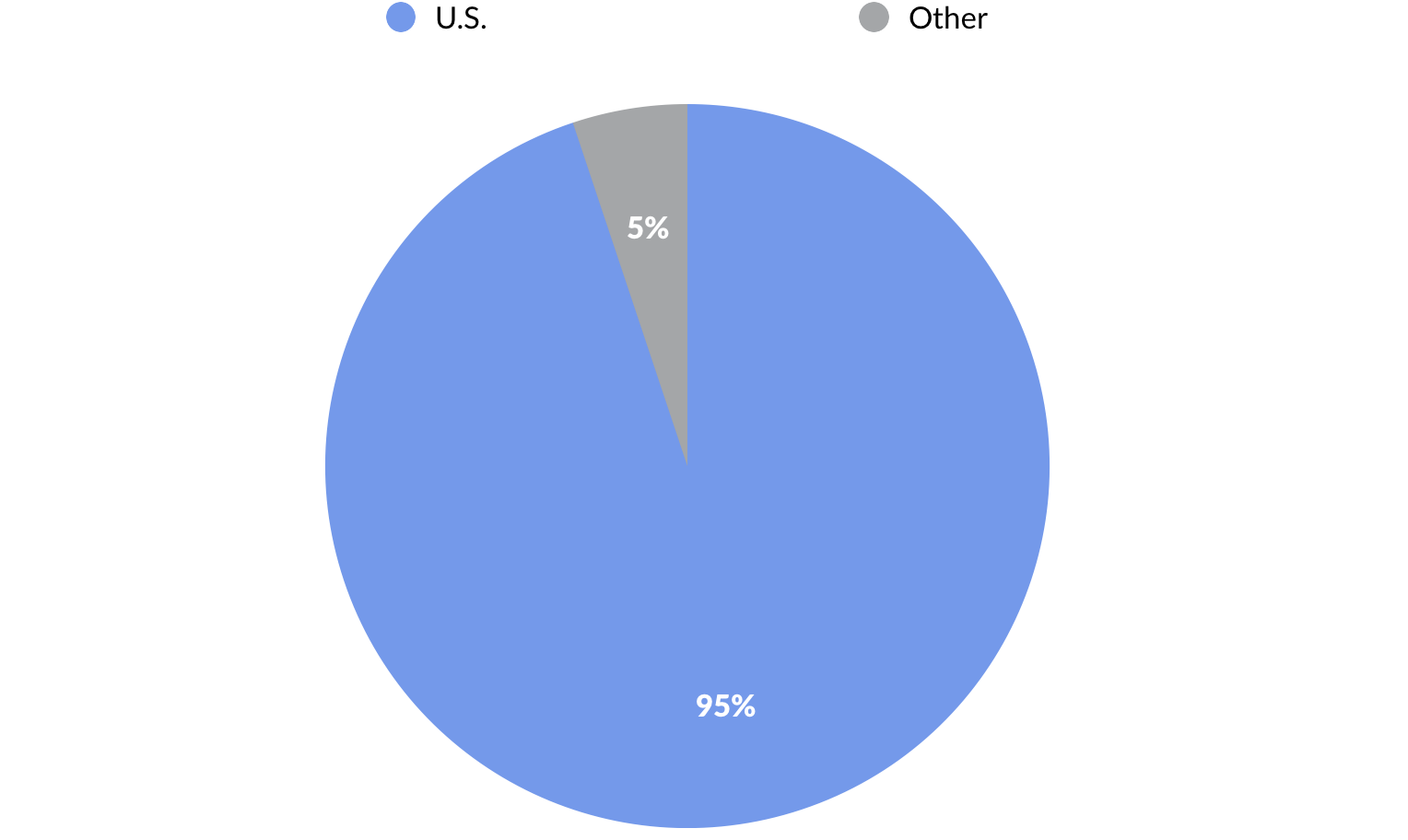

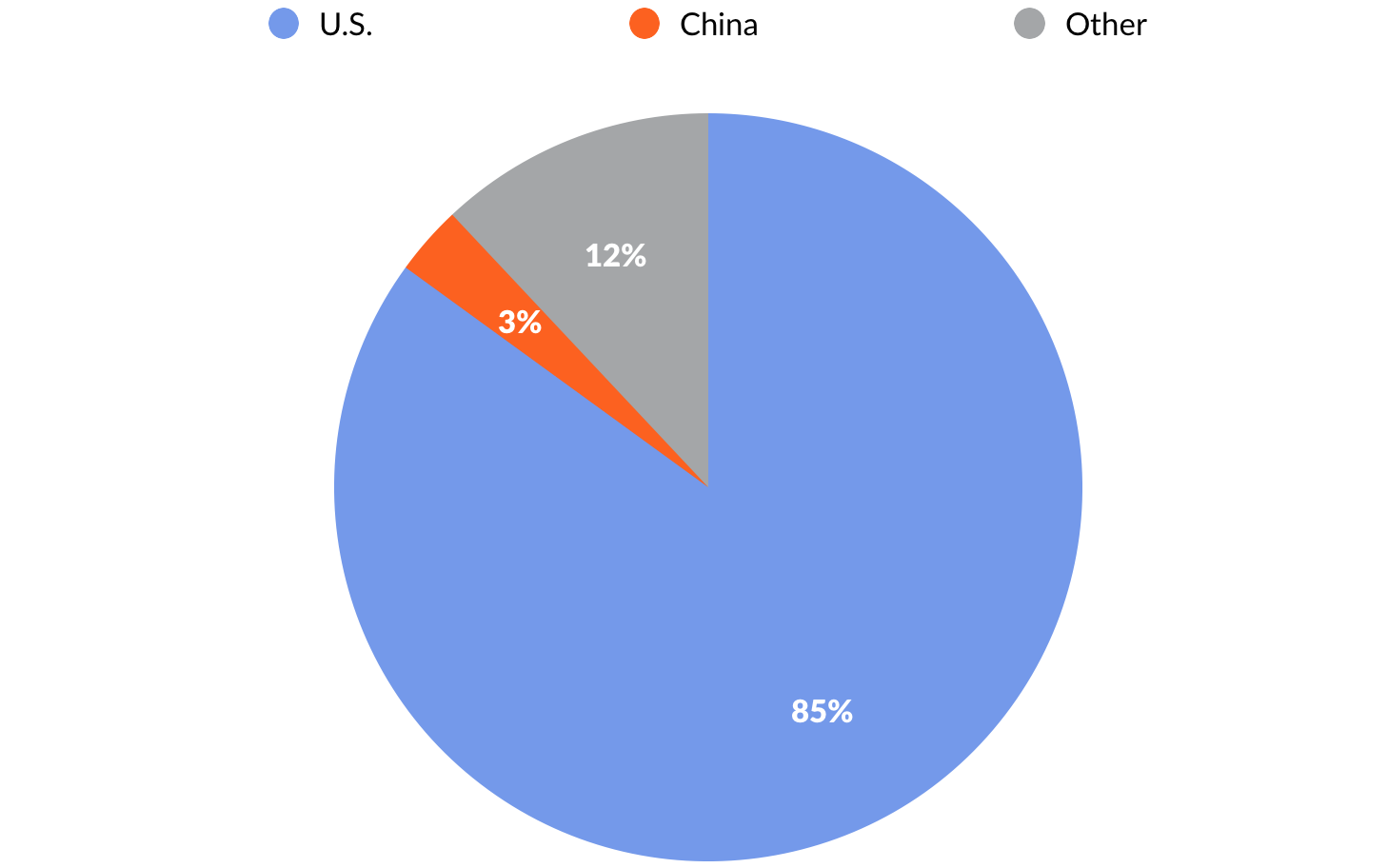

Looking at the GSV 300 by geography, 38% of the index weightage comes from U.S. companies. China is the second-largest geography at 18%, followed by India at 14%, and Indonesia and South Korea at 3%. By contrast, 95% of the S&P 500 and 85% of NASDAQ are represented by U.S. companies.

NASDAQ BREAKDOWN BY COUNTRY

GSV 300 UPDATE: Q2 2017

The GSV 300 has roared up 26.6% year-to-date, gaining 8.5% in the second quarter. While we were pleased with the strong performance, our objective in launching the index was to create a scorecard that reflects what is actually going on in the World of growth stocks. The real insight is in the metrics.

Segmented by country, second quarter growth was led by Chinese companies, which gained 9%. Indian and U.S. companies rose 8% and 7%, respectively.

Segmented by GSV investment theme, “Marketplace” enterprises recorded the highest gains, rising 25% for the quarter. “Social/Mobile” companies were up 13%, “Cloud + Big Data” companies were up 9%, and “Sustainability” and “Education Technology” companies were up 8% and 7%, respectively.

We will continue to root for strong performance. But our goal with each passing quarter is to develop a data set that becomes a barometer for growth, especially when comparing the fundamentals of the GSV 300 to traditional indices.

The T. Rowe Price New Horizons Fund, for example, has pursued a strategy of investing in small, high-growth companies since 1961. While it is actively managed, Peter Lynch observed in Beating the Street that the fund is, “as close as you’ll get to a barometer of what is happening to emerging growth stocks.”

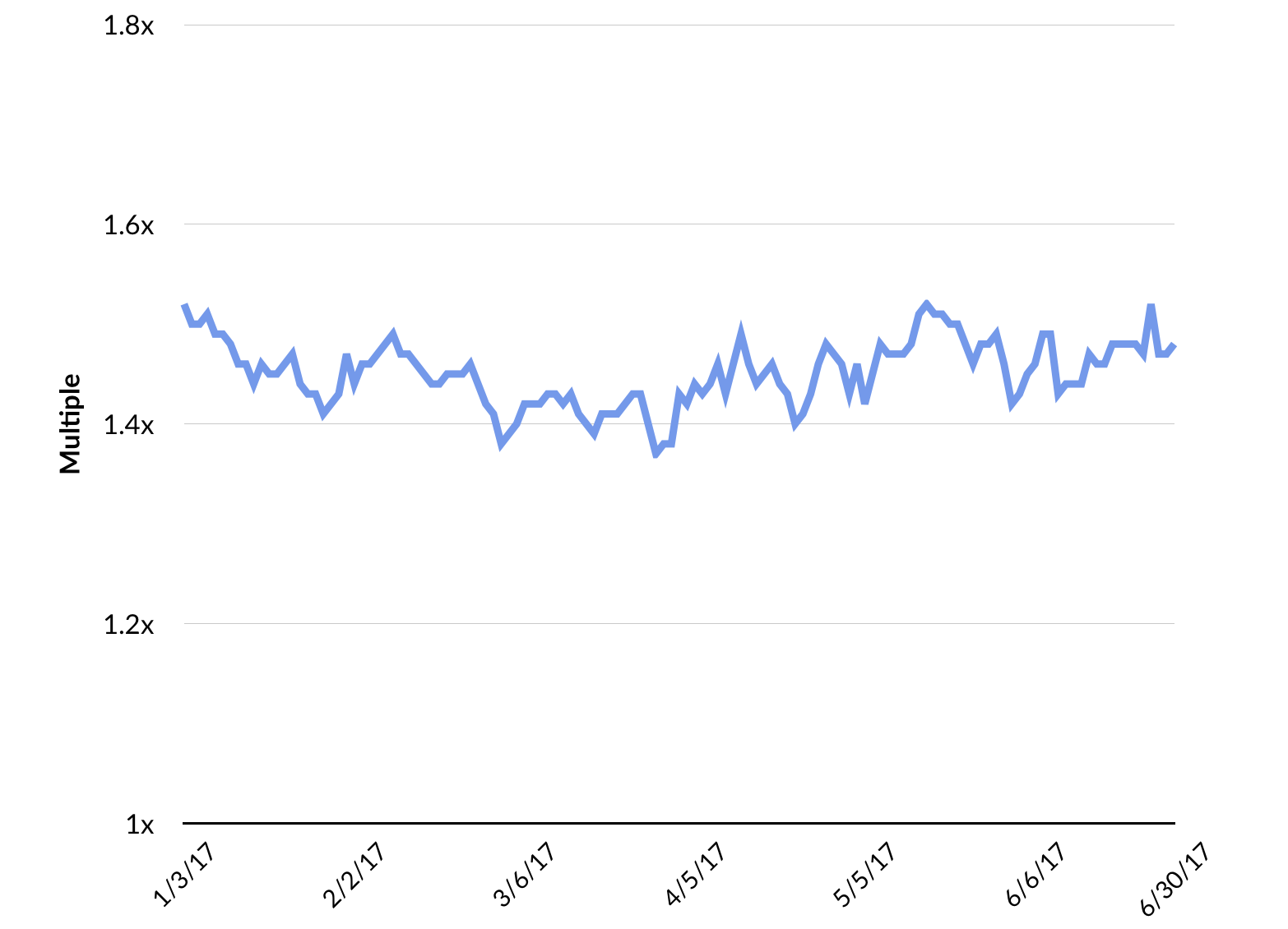

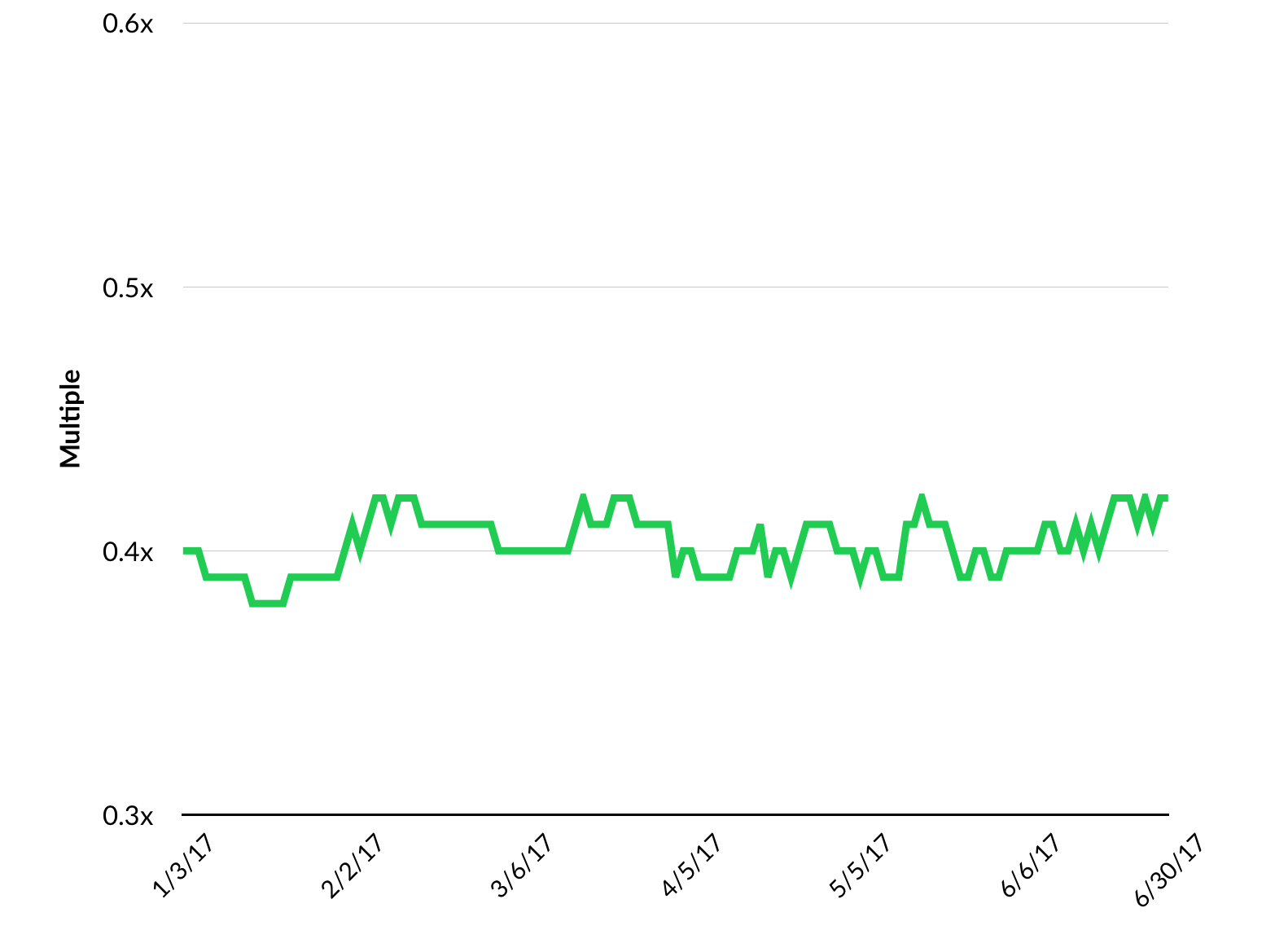

Since small companies are expected to grow at a faster rate than large companies, they usually sell at a higher P/E than larger companies. Logic might suggest, therefore, that the P/E of the New Horizons Fund would be higher than that of the S&P 500 at all times.

This isn’t always the case, and at times when it isn’t, the New Horizons Fund can be a smoke signal for an undervalued or overheated growth economy. Over the last 50 years, for example, the New Horizons P/E has risen to double that of the S&P 500 only four times.

Currently, the GSV 300 has a P/E (forward) of 26.9, or 1.5x greater than the S&P 500. Our thesis is that at over 2x, it’s a warning signal for growth stocks, and at under 1.2x, it’s a buying opportunity. We will continue to monitor this trend, as well as the relationships of other key valuation metrics, to determine patterns over time.

IPO UPDATE: Q2 2017

Through the end of Q2, there were 72 IPOs — 28 VC-backed — generating an average of $245 million in proceeds. Twelve companies priced above range, 40 priced in range, and 20 priced below. The average one-day pop was 8%.

April had two notable technology IPOs with both Okta and Yext going public, popping 38% and 22% respectively. Founded in 2009, enterprise cloud security startup Okta had VC backers including Andreessen Horowitz, Sequoia Capital, and Greylock. Yext lets businesses like BMO Harris Bank, Marriott, and Ben and Jerry’s manage their digital knowledge in the cloud and syncs it to over 100 services, including Apple Maps, Google, Instagram, Siri and Yelp.

Recipe and food delivery service Blue Apron went public late last week, pricing at the low end of its offering and trading flat. The company slashed its IPO offering price from $15-17 to $10 following the announcement of the Whole Foods and Amazon acquisition. The company has delivered over 159 million meals and recipes to date and its investors included Bessemer, First Round, and Fidelity. Blue Apron has fallen going public, down nearly 20% since last week.

Also going public late last week, food delivery service Delivery Hero made its debut on the Frankfurt Stock Exchange, popping 11%. Backed by Rocket Internet, Delivery Hero is available across 42 countries and counts 150,000 restaurants as partners in its network. Delivery Hero’s investors alongside Rocket Internet included Insight Venture Partners, Naspers and Holtzbrink.

Source: GSV Asset Management

Disclosure: GSV owns shares in Lyft

Real estate startup Redfin filed for an $100 million IPO with Goldman Sachs as their lead banker. Based in Seattle and founded in 2004, Redfin has raised $186 million to date from investors including Madrona, DFJ, T. Rowe Price, and Wellington. Redfin was last valued at $500 million in 2015.